Explore finance

Stay one step ahead in the world of cryptocurrencies, forex, stocks, indices and commodities: read the latest news and expert opinions!

ARTICLES & NEWS

Our articles on markets analytics & tech

03.07.2026

Bitcoin climbs above $61,000 as weak US jobs data fuels Fed rate cut hopes

Market Update: Bitcoin and Ethereum Make Significant Gains

The cryptocurrency market witnessed substantial movement during the past 24 hours, with Bitcoin climbing by 2.80% and reaching a trading value of $61,739, and Ethereum increasing by 6.24% to stand at $1,716. Among the major altcoins, BNB, XRP, Solana, Tron, Hyperliquid, Dogecoin, and Cardano saw gains of up to 6.68%. These movements are likely influenced by macroeconomic factors, particularly the release of weaker U.S. job numbers, which have heightened expectations of a potentially less restrictive stance by the Federal Reserve.

Analysis of the Cryptocurrency Surge

The potential for further gains in Bitcoin remains, according to Riya Sehgal, a Research Analyst at Delta Exchange. She highlights that the current movement should be interpreted as a relief rally rather than a confirmed trend reversal. With the first significant resistance point for Bitcoin at $62,200, overcoming this threshold could pave the way for further growth toward $64,000-$65,000.

ETF Flows and Institutional Demand

The uneven flows in Bitcoin ETFs contrast with the relatively flat performance of Ethereum ETFs. While Bitcoin's recent uptick to $62,000 was bolstered by large-scale purchases of 270,000 BTC by whales, it also inflicted substantial losses on short positions amounting to $130 million. Meanwhile, the Fear and Greed Index experienced an increase, indicating an improvement in market sentiment, yet fear still prevails according to the CoinDCX Research Team.

Global Crypto Market Capitalisation

The broader cryptocurrency market has seen its total capitalisation rise by 2.64%, reaching $2.13 trillion as reported by CoinMarketCap. During the last week, both Bitcoin and Ethereum have achieved notable gains of 1.97% and 8.68% respectively. Among the altcoins, XRP, Solana, Hyperliquid, Dogecoin, and Cardano rose by up to 14.91%, while BNB and Tron witnessed minor declines.

Market Outlook: Short Squeeze and Long-term Conditions

CoinSwitch Markets Desk attributes Bitcoin's rebound toward the $62,000 mark primarily to a short squeeze. Despite this, the broader market outlook remains mixed, with weak institutional demand and competing pressures from higher bond yields. The forthcoming major price movement in Bitcoin will likely depend on a convergence of macroeconomic conditions, institutional involvement, and Bitcoin's ability to sustain a position above the $62,000 threshold, potentially reaching the $65,000 resistance level.

Experts' Perspectives on the Recent Market Developments

Avinash Shekhar, Co-Founder & CEO of Pi42, elaborates on the current market dynamics, noting how Bitcoin's recovery reflects its sensitivity to macroeconomic expectations following weaker U.S. jobs data. He suggests that the investment narrative is shifting from fears of precipitous price drops to considerations on the return of market liquidity.

Nischal Shetty from WazirX and Vikram Subburaj from Giottus provide further insights. Shetty points to Bitcoin's strength at surpassing the $60,000 barrier as a positive investor reaction to the anticipated monetary policy easing, while highlighting increased interest in Ethereum ETFs. Subburaj observes the stabilization of market sentiment following Bitcoin's previous dip to $58,000, yet hesitates to predict a full trend reversal.

Akshat Siddhant, Lead Quant Analyst at Mudrex, remarks on the increased exchange inflows for Bitcoin and Ethereum, highlighting a level of activity that often precedes heightened volatility, as previously seen in the June downturn to $58,000.

The evolving cryptocurrency landscape remains subject to diverse influences, from macroeconomic developments to institutional activity, indicating the need for continuous vigilance and analysis to navigate future trends effectively.

01.07.2026

Bitcoin price breakout above $60K lacks fresh buying fuel: analyst

Bitcoin's Struggle Below $60,000: A Reflective Analysis of Market Dynamics

Bitcoin, the leading cryptocurrency, once again finds itself in a precarious position as its price dips below the psychologically significant $60,000 threshold. After several attempts to break out, the digital asset remains under pressure, illustrating the complexities of current market conditions. With weak stablecoin inflows exacerbating concerns about insufficient fresh buying momentum, investors and traders are left questioning the potential for a sustainable upward trajectory.

Challenging Market Conditions and the Role of Stablecoins

The market sentiment surrounding Bitcoin remains subdued due to a confluence of factors. Central among these is the weakening of stablecoin inflows, a critical metric as stablecoins often act as a primary conduit for new capital entering the cryptocurrency markets. According to data insights from crypto.news, Bitcoin's flirtation with the $60,000 mark on June 30 was short-lived, as it quickly fell back to around $59,300, extending a series of unsuccessful breakout attempts since dropping below that level on June 25.

On-chain data analyzed by CryptoQuant analyst Sunny Mom reveals a dearth in the influx of new capital essential for fueling a sustained breakout. Significantly, the 30-day stablecoin market capitalization growth rate has seen a downturn. Both USDC issuance and the growth of Ethereum-based USDT have shown signs of deceleration. The scarcity of new stablecoin issuance stands as a barometer indicating that investors are hesitating to convert fiat currencies into digital assets.

Institutional Trading Patterns and Macro Headwinds

In conjunction with dwindling stablecoin supplies, the institutional landscape further compounds Bitcoin's challenged rally. Data points to nearly $1.79 billion in net outflows from U.S. spot Bitcoin exchange-traded funds during the final week of June, marking a significant reduction in one of the key channels for spot Bitcoin demand. Institutional selling has been buoyed by processes such as quarter-end portfolio rebalancing and certain strategic initiatives like Strategy's Digital Credit Capital Framework. This ongoing supply-release to meet redemptions and obligations continues to exert downward pressure on Bitcoin's price.

The macroeconomic environment has not been favorable either. Economic indicators such as the U.S. Core PCE inflation suggest a postponement of anticipated Federal Reserve rate cuts, nudging investors towards more stable fixed-income assets. In parallel, developments in global oil markets and geopolitical engagements, notably the U.S.-Iran negotiations, have kept financial markets on alert, fostering a climate of caution adverse to high-risk ventures.

Technical and Momentum Analysis: A Cautious Outlook

From a technical perspective, Bitcoin's structure presents an outlook that favors a continuation of selling pressure. The cryptocurrency trades just above pivotal support around $58,169, which aligns with the 100% Fibonacci retracement of its recent decline. A breach below this support level could pave the way for further retreats into the mid-$50,000s.

Momentum readings have yet to signal a substantial recovery, with indicators such as the Relative Strength Index (RSI) hovering near oversold zones and the MACD still beneath the zero line. Although selling momentum appears to have abated, buying forces are yet to assert dominance effectively.

Derivative market dynamics also hint at potential volatility. Notably, CoinGlass data outlines significant downside liquidity clusters between $58,800 and $59,000, alongside leveraged positions that could exert influence around $61,000 to $61,500.

Future Prospects: Navigating Through Uncertainty

As Bitcoin hovers in this critical price corridor, its immediate future hinges on the robustness of the $58,000 to $59,000 support zone. Analyst Ted Pillows emphasizes this range as a vital threshold for any semblance of a rally. A defense of this zone could spur a corrective bounce, potentially propelling prices back to the low $60,000s, contingent on an alleviation in selling pressure.

However, persistently weak stablecoin activity, ETF redemptions, and macroeconomic uncertainties could continue to amplify bearish sentiment. Investors and traders must remain vigilant and strategically adaptive to navigate this evolving landscape, as Bitcoin's journey below and above $60,000 remains a central focus in the ongoing discussions about the cryptocurrency's future trajectory.

29.06.2026

Why Bitcoin Just Hit a 20-Month Low -- What Comes Next

Bitcoin Hits a 20-Month Low: Market Analysis and Community Insight

In the past few days, Bitcoin has plummeted to a concerning 20-month low, setting the trading community abuzz with active discussions. This decline, detailed in the recent Solana Weekly News Recap, was marked by the liquidation of $1.2 billion in positions. As traders dissect the implications of this event, many are left questioning whether this marks the nadir for Bitcoin's price trajectory. This situation unfurls against a backdrop of broader market dynamics that continue to exhibit mixed signals. Let us delve into the current scenario and its possible implications for traders and investors alike.

The Story So Far

The Bitcoin ecosystem stands at a crucial threshold, underscored by its recent descent to a 20-month low. The influential Tweet from SolanaFloor highlighted the context surrounding this decline, specifically emphasizing the $1.2 billion in liquidations. This significant market activity has stirred discussions about the possible reversal of this trend, with traders and investors alike evaluating whether Bitcoin's current position might signal a buying opportunity or hint at a continued bearish trajectory. The trading landscape is fraught with uncertainty, leading many to ponder what lies ahead for Bitcoin and the broader cryptocurrency market.

At a Glance

Bitcoin's recent decline has catalyzed considerable discussion among traders, reflecting a growing apprehensiveness within the crypto community. The market's fluctuations are noteworthy, showcasing an interplay of caution and speculation that underscores the current sentiment. The significant $1.2 billion liquidation underscores the volatility that has gripped the market. As Bitcoin hovers at this pivotal low point, trading volumes remain muted, indicative of a collective lack of conviction among market participants.

By the Numbers

Amid the current market dynamics, Bitcoin's position is indicative of broader trends within the cryptocurrency sphere. Historically, Bitcoin has wielded considerable influence within the crypto market, often serving as a bellwether for other digital assets. Recent events, including substantial liquidations and widespread community discussions regarding its price direction, underscore the interconnected fabric of cryptocurrency trading. As traders navigate this intricate landscape, grasping the overarching trends and discerning sentiment within the community becomes essential to crafting informed and strategic decisions.

What to Watch

In the days ahead, traders are advised to closely observe Bitcoin's price movements and the evolving market sentiment. With potential for further volatility, the identification of key levels of support and resistance will serve as critical indicators for navigating the market's ebbs and flows. Furthermore, ongoing community dialogues and expert analyses will likely shed light on the prevailing sentiment, aiding traders in shaping effective strategies as Bitcoin's journey continues to unfold.

As always in the domain of cryptocurrency investments, it is crucial to acknowledge the high risks and volatility inherent in this space. Traders and investors must conduct thorough research and seek guidance from financial advisors to make well-informed investment decisions. Navigating the turbulent waters of the cryptocurrency sea demands vigilance, strategy, and a pulse on both market dynamics and community sentiment.

26.06.2026

BYDFi Referral Code dwPtzS - Benefits, Trading Features, and Registration Guide for USA & EU Users in 2026

The Expanding Cryptocurrency Trading Industry

The cryptocurrency trading industry continues to thrive as investors worldwide search for reliable, efficient, and feature-rich platforms for buying and trading digital assets. A noteworthy player in this evolving market is BYDFi, a global cryptocurrency exchange garnering international attention, including in regions like the United States and European Union, where operations are subject to local regulatory permissions.

Leveraging the BYDFi Referral Code dwPtzS

New users looking to maximize their experience on BYDFi can benefit from using the BYDFi Referral Code dwPtzS during the registration process. Eligible users might qualify for promotional rewards worth up to $8,100 USDT, subject to campaign stipulations, completed tasks, and trading activity.

Understanding the BYDFi Referral Code

Rather than functioning as a simple discount mechanism, the BYDFi Referral Code dwPtzS connects new users to the exchange's welcome rewards program. This article delves into the mechanics of the referral code, its associated benefits, the registration process, and the growing popularity of BYDFi among cryptocurrency traders ranging from novices to seasoned professionals.

Why BYDFi Is Gaining Popularity Among Global Traders

In the highly competitive cryptocurrency exchange landscape, traders demand more than just low trading fees. Key differentiators now include platform security, asset liquidity, supported cryptocurrencies, user experience, diverse trading tools, and attractive promotional programs.

BYDFi has strategically positioned itself as a user-centric cryptocurrency exchange, emphasizing accessibility with a clean interface and an expanding array of trading products. Its platform supports users worldwide, offering services to both entry-level and professional traders.

Simplifying Cryptocurrency Trading

BYDFi's commitment to simplifying cryptocurrency trading is evident through its easy-to-navigate account management and advanced trading tools. Users can start with basic spot trading and gradually explore the more complex futures markets and other investment opportunities. This layered approach enhances the platform's appeal among both beginner and experienced traders.

Enhanced Accessibility in the USA and European Union

Recognizing the importance of accessibility in key markets such as the USA and European Union, BYDFi is continuously improving its platform infrastructure, security measures, and promotional endeavors aimed at attracting new account holders.

How the BYDFi Referral Code dwPtzS Works

The BYDFi Referral Code dwPtzS serves as a registration code for new users interested in joining the BYDFi platform. Unlike typical promotional coupons that provide immediate cash rewards, this referral code acts as an identifier, enrolling new accounts into the exchange's welcome campaign. The rewards can include welcome bonuses, trading vouchers, futures bonus credits, fee discounts, among other incentives, depending on the campaign specifics.

Important Registration Steps

Entering the BYDFi Referral Code dwPtzS during account creation is crucial. Many exchanges do not offer the ability to add referral codes post-registration, making it imperative for users to take this step during account setup to qualify for promotional opportunities.

Step-by-Step Registration Process

Registering on BYDFi involves several key steps:

Step 1: Create a New BYDFi Account

Begin by visiting the official BYDFi registration page and opt for registration via email or mobile number.

Step 2: Enter the Referral Code

During registration, input the BYDFi Referral Code dwPtzS in the designated field, linking your account to the applicable welcome promotion.

Step 3: Verify Your Account

Complete the necessary email or mobile verification processes. Depending on location and campaign requirements, identity verification (KYC) might be needed to access additional account features and higher reward tiers.

Step 4: Secure Your Account

Prior to your initial deposit, enable Two-Factor Authentication (2FA), craft a robust password, and review the available security settings.

Step 5: Complete Eligible Activities

After registration, users may need to fulfill activities such as initiating a deposit, executing their first trade, participating in spot or futures markets, completing promotional tasks, and achieving set trading volume targets to unlock different reward levels.

Decoding the "Up to $8,100 USDT" Reward

New users often wonder about the "up to $8,100 USDT" reward. It's important to understand this figure represents the maximum promotional value obtainable through the campaign rather than a guaranteed payout upon signup. BYDFi typically distributes rewards over multiple stages, including account registration, identity verification, first deposit, trade completion milestones, and more.

Trading Products on BYDFi

BYDFi attracts traders due to its comprehensive portfolio of trading services, including:

Spot Trading

Spot trading enables users to buy and sell cryptocurrencies at prevailing market rates, catering to both long-term investors and active day traders.

Futures Trading

Futures trading offers greater flexibility by allowing users to speculate on market movements, employing leverage when available for amplified profit potential, albeit with heightened risk.

Copy Trading

Beginners can explore copy trading, following experienced traders whose portfolios are mirrored automatically. It's essential to remember that past performance doesn't guarantee future outcomes, necessitating a thorough risk assessment.

Advantages of the BYDFi Referral Code dwPtzS

The BYDFi Referral Code dwPtzS presents numerous advantages, primarily providing access to exclusive promotional campaigns unavailable to non-referred accounts. The code seamlessly integrates accounts into welcome reward programs from the outset, potentially offering trading vouchers, bonus credits, or reduced fees, thus lowering initial trading expenses.

Is BYDFi Suitable for Beginners?

BYDFi is crafted to cater to both beginners and seasoned traders alike. Newcomers benefit from a simple registration process, user-friendly interface, and educational resources that demystify complex cryptocurrency concepts. Simultaneously, experienced traders can enjoy futures markets, a vast array of cryptocurrencies, and additional trading tools.

Final Thoughts

The BYDFi Referral Code dwPtzS offers eligible newbies a gateway to BYDFi's rewarding welcome campaigns, potentially yielding promotional bonuses up to $8,100 USDT. Instead of offering an immediate cash bonus, the referral code guides new accounts into a structured rewards framework that may involve trading bonuses, promotional vouchers, and activity-based rewards.

Beyond referral campaigns, BYDFi is establishing itself as a notable global cryptocurrency exchange, providing spot and futures trading, copy trading, and a user-friendly platform accessible to users from multiple regions, including eligible traders in the USA and European Union.

Prospective users should always evaluate the latest promotional terms, ensure all required verifications are completed, and comprehend any attached conditions for reward campaigns. By analyzing the platform based on security, trading features, liquidity, user experience, and beyond promotional incentives, traders can assess whether BYDFi aligns with their investment objectives in 2026.

Related Items

BYDFi Referral, Trading Features

24.06.2026

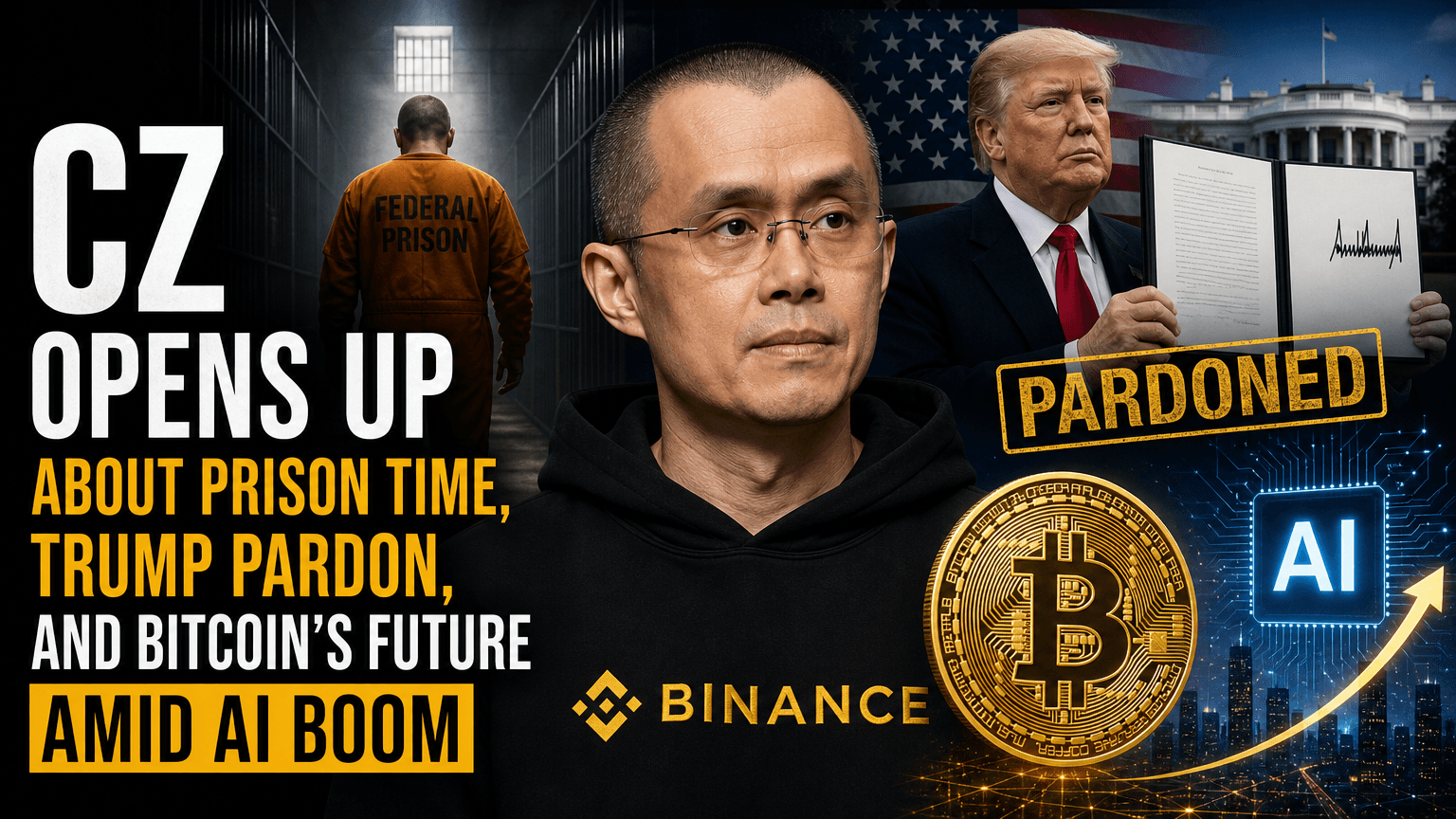

CZ Opens Up About Prison Time, Trump Pardon, and Bitcoin's Future Amid AI Boom

Changpeng Zhao's Journey: From Incarceration to Rebuilding a Billion-Dollar Vision

Changpeng Zhao, widely known in the cryptocurrency world as CZ, has openly shared his experiences from the time he spent behind bars, his subsequent presidential pardon, and his promising outlook on how the growth of artificial intelligence can positively influence the cryptocurrency sector. As the co-founder of Binance, the world's largest cryptocurrency trading platform, CZ boasts an estimated fortune of approximately $110 billion as per Forbes, ranking him among the top 20 wealthiest individuals globally.

Legal Challenges and Presidential Pardon

CZ's legal troubles stemmed from an extensive investigation by the U.S. Department of Justice. Authorities accused him of operating a financial services platform that did not implement adequate anti-money laundering protocols. In November 2023, CZ pleaded guilty to these charges and subsequently stepped down as the CEO of Binance. After serving a four-month federal prison sentence, CZ regained his freedom in September 2024.

In a turn of events, on October 23, 2025, former President Donald Trump granted CZ a full pardon, describing the prosecution as part of the Biden administration's alleged "war on cryptocurrency." CZ mentioned his intention to personally thank Trump for the pardon. The incident highlights ongoing tensions and differing views on cryptocurrency regulation between various political entities.

Rebuilding After Incarceration

Reflecting on his time in prison, CZ disclosed on the Power Players podcast that the mental burden of incarceration far outweighed the physical hardships. "Numerous prominent media organizations reported that I would become the wealthiest individual ever incarcerated in a U.S. federal facility," he recounted. "My legal team warned me that I would likely be a prime target for extortion schemes." This newfound perspective fueled his drive to rebuild and refocus his efforts post-incarceration.

In the aftermath, CZ took several weeks to adjust and regain momentum. He delineated three primary areas of focus for his future endeavors: supporting transformative technology entrepreneurs, advising governments on cryptocurrency policy frameworks, and expanding his educational initiative, Gig Academy. The academy aims to empower learners by providing free access to cutting-edge education in digital finance, with enrollments skyrocketing from 100,000 to 500,000 students in the past six months.

CZ's Perspective on Cryptocurrency and Artificial Intelligence

CZ maintains an optimistic outlook on the future of cryptocurrency, considering Bitcoin's price point of $60,000 as "really low" compared to its historical peaks. "During the previous winter, it traded at $16,000," he observed, highlighting the market's potential for growth through enhanced applications and practical use cases.

Furthermore, CZ views the current wave of investments in artificial intelligence as an opportunity rather than a threat to cryptocurrency. As more investors explore digital assets to enter AI-focused ventures, trading activity and market engagement are expected to increase. He forecasts a future where AI agents autonomously handle payments and transactions through cryptocurrency systems within months.

Drawing a parallel to the evolution of the internet, CZ believes that blockchain technology will not be overshadowed by AI, reminiscent of how the web remained vital despite blockchain advancements. He anticipates that investments currently funneled into artificial intelligence will eventually flow back into blockchain infrastructure, encouraging greater integration between these transformative technologies over the coming years.

Although both industries will likely encounter regulatory hurdles and technical challenges, CZ remains steadfast in his commitment to long-term development goals, setting the stage for a future where innovative tech entrepreneurs can thrive under his guidance. This vision underscores an optimistic horizon for digital assets, poised for renewed growth and unprecedented applications.

22.06.2026

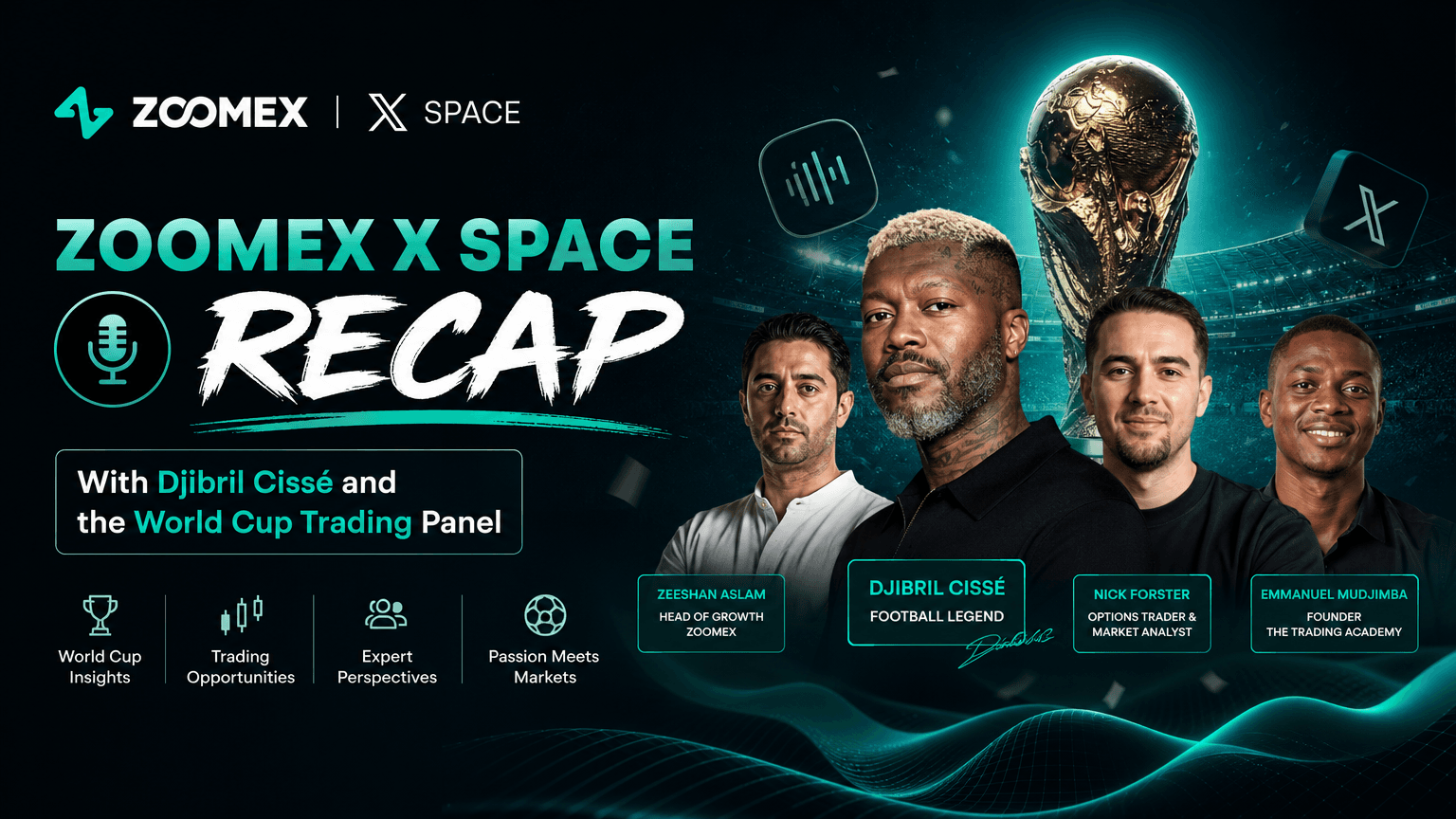

Zoomex X Space Recap With Djibril Cissé and the World Cup Trading Panel

Confidence and Decisions: Insights from Djibril Cissé

Djibril Cissé, known for his exploits both on and off the football field, provides a fascinating insight into the psychological game underpinning high-stake scenarios. The former footballer posits that the critical distinction between confidence under pressure and paralysis is the personal desire to take responsibility for the outcome. Cissé’s philosophy resonates not only in sports but also in the realms of trading and finance, where decision-making under pressure is paramount.

Philosophy of Resilience: Turning Setbacks into Opportunities

Throughout his career, Cissé has faced numerous challenges, including severe leg injuries and missing major tournaments. Despite these setbacks, his approach has been consistent: instead of focusing on missed opportunities, he emphasizes working with what is available. This mindset is invaluable in trading, where market conditions and outcomes are often unpredictable. A trader's resilience comes from the ability to move forward using available information, adapting strategies according to the landscape.

Timing as the Real Edge in Trading

The panel of traders during the Zoomex World Cup Edition highlighted that timing really is the crucial factor in trading. However, how timing is defined greatly depends on the timeframe in which one operates. Whether you are a day trader focusing on minute-by-minute movements or a long-term investor gauging trends over weeks or months, timing plays a different role. This continuous assessment can be likened to a striker considering the right moment to strike in soccer; different timelines, same critical step.

Zoomex World Cup Edition: Combining Football and Cryptocurrency

Zoomex brought together an eclectic mix of Champions League winner Djibril Cissé and four crypto traders for a discussion filled with football analysis, trading philosophies, and more. This session is the first of five episodes as part of their World Cup Impact Pledge, aimed at marrying sports with charitable contributions. Zoomex's commitment to using the platform for good is evidenced by its promise of donating 1,000 USDT per episode to a charity of the football guest's choice, with opportunities for larger contributions based on World Cup predictions.

Courage Under Pressure: Lessons from Cissé and Traders

At the heart of Cissé’s commentary and trader insights is the management of pressure. For Cissé, the pressure before taking a penalty, much like a trader’s instinct before executing a large position, isn't overwhelming — it's anticipated. Both fields require rigorous preparation and comfort with one's systems. Professional traders, similar to athletes, must harness their environments for predictability, minimizing uncertainty through prepared strategies.

The Right Timing and Execution Speed in Trading

During the session, the panel pondered whether speed of execution or timing of entry mattered more. Timing emerged as the clear winner, with Bitsofwealth wisely noting that whether you are too early or too late, the result can remain equally unsatisfactory. The merit of timing is adaptive; it shifts based on one’s strategy and timeframe. Just as a striker like Cissé must choose the right moment to exploit, so must traders identify the correct conditions for their entries.

The Importance of Mindset: Adapting to Injuries and Setbacks

Injuries marked Cissé’s career, yet his recovery philosophy echoes essential trading wisdom. Understand the situation, recognize the loss, and adapt strategically rather than emotionally. As Bitsofwealth noted, less than one percent of traders succeed consistently by understanding and learning from their mistakes. Here lies Cissé's enduring lesson: each setback is informative, a point of leverage for future improvement.

Understanding Challenges from a Strategic Perspective

Cissé’s reflections on his toughest opponents further emphasize the necessity of adapting to circumstances — a tenet echoed in trading. Adapting to counter strategies by recognizing potential threats mirrors how traders need to adapt to evolving market conditions, sometimes even foreseeing potential hurdles before their impacts fully manifest.

The Futility of Regretting What Never Happened

When asked about hypothetical scenarios, such as whether France could have won the 2006 World Cup with him on the team, Cissé demurred, pointing out the futility of speculating on events that never transpired. This pragmatic view applies to trading where fixating on missed opportunities doesn't facilitate growth. Rather, focusing on actionable insights from real events helps traders refine their strategies.

Potential Future Stars and the Landscape of National Teams

Cissé spotlighted emerging football talents and noted the merit in paying attention to underdog stories. Within these narratives lies a deeper lesson applicable to market trends — sometimes true potential is hidden in plain sight, and recognizing emerging capabilities before they become apparent to everyone can offer a real edge.

Mapping Cryptocurrencies to National Teams

In a lighter vein, the session explored analogies between cryptocurrencies and national football teams, sparking both laughter and insights. Such comparisons illustrate the communal aspects of both fields — the fanbases, the hype cycles, and the lessons in reliability and consistency. Discussions around Bitcoin being akin to football powerhouses capture how cryptos are perceived in terms of longevity and core reliability.

Concluding Thoughts and Lessons from the Zoomex Space

The session underscored that whether in sports or trading, navigating pressure and making decisions in uncertain times define success. Understanding how to operate when risks are evident offers not just a survival mechanism but also a framework for leverage over time.

About Zoomex and Its Values

Zoomex represents a forward-thinking cryptocurrency exchange platform, fostering a transparent and user-centric environment. Apart from operational excellence, its commitment to community and social values through initiatives like the World Cup Impact Pledge positions it as a facilitator of both financial and social capital.

19.06.2026

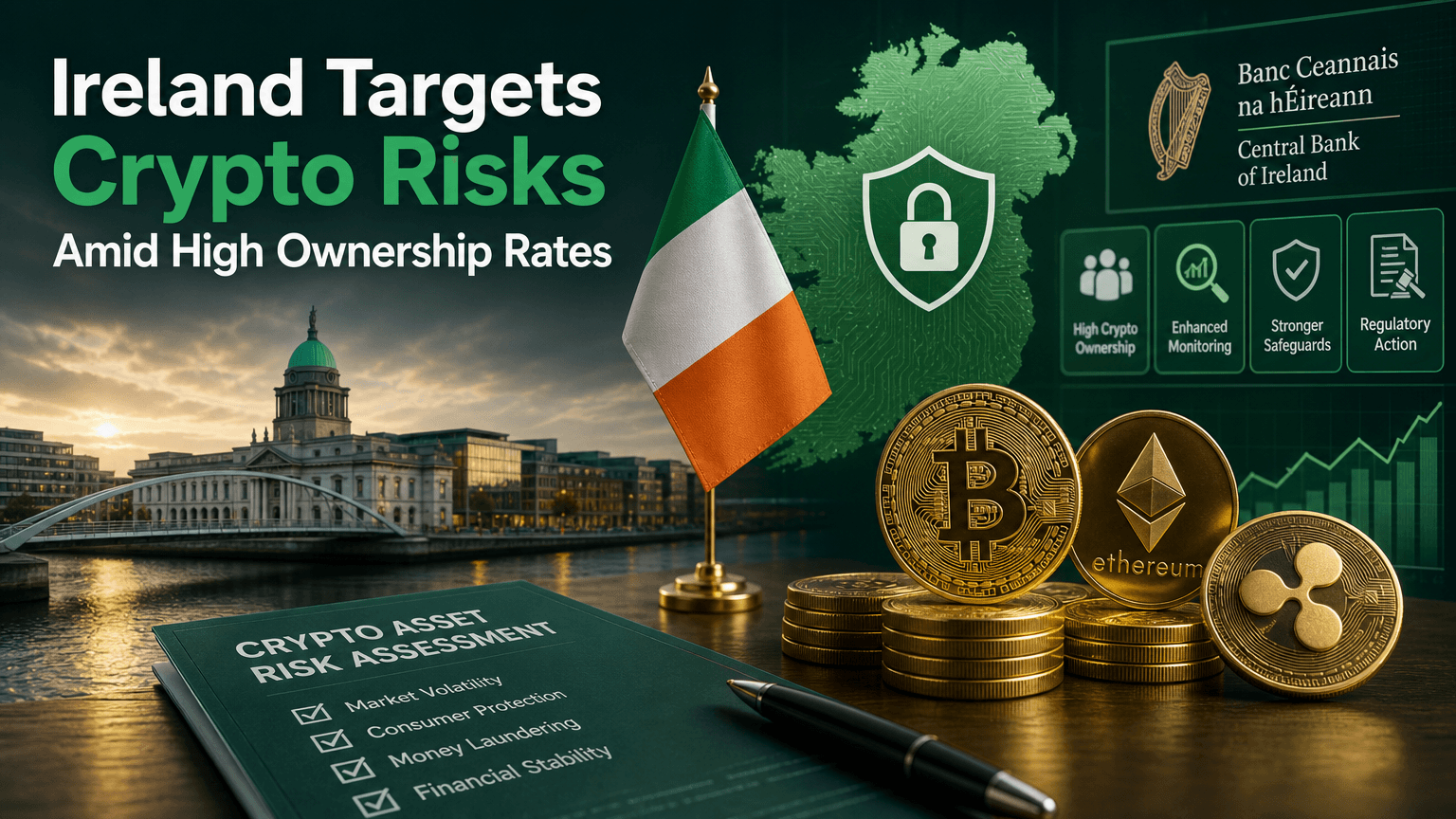

Ireland Targets Crypto Risks Amid High Ownership Rates

Ireland's Comprehensive Digital Asset Risk Assessment

For the first time in seven years, Ireland has released a comprehensive risk assessment on digital assets, highlighting vulnerabilities like money laundering, terrorism financing, and sanctions evasion. This significant announcement coincides with the Irish government's plan to implement stricter safeguards for crypto-related activities by the second half of 2027.

The report, published on June 18, identified crypto assets as posing "very significant" risks in the realm of financial crime. Additionally, it highlighted challenges associated with decentralized finance (DeFi) and inconsistent international regulations. The Irish Department of Finance emphasized the attractiveness of cryptocurrencies to criminal groups, citing its use in bribery cases and tax evasion schemes. This development marks a shift towards more proactive regulation in a country where approximately 10% of the population owns cryptocurrencies, as reported by the Central Bank of Ireland in December 2025.

High Adoption, Limited Oversight

Ireland boasts one of the highest crypto ownership rates in Europe, surpassing the OECD average of 3.8%. This impressive retail participation contrasts starkly with the country's relatively underdeveloped regulatory framework. Although the EU's Markets in Crypto-Assets (MiCA) regulation has been in effect since late 2024, Ireland's enforcement of these rules is still a work in progress. Under MiCA, Crypto-Asset Service Providers (CASPs) are required to be authorized and supervised by national regulators, including Ireland's Central Bank.

Recent enforcement actions have exposed gaps in compliance. For instance, in November 2025, Coinbase Europe Limited was fined €24 million for delays in addressing anti-money laundering (AML) violations. Furthermore, Ireland's Criminal Assets Bureau seized €30 million in cryptocurrency in March 2026, highlighting the scale of illicit activity associated with digital assets.

Upcoming Policy Changes

The Irish government is planning to introduce industry standards by 2027 to address the risks identified in its latest assessment. These measures will likely align with broader EU initiatives like DAC8 and the Common Reporting Standard for Crypto-Asset Reporting Framework (CARF), which require crypto exchanges serving EU users to automatically report transaction data for tax purposes. These rules, effective from January 2026, are designed to close loopholes that facilitate tax evasion and enhance transparency across the sector.

Ireland has already adopted a stringent approach to cryptocurrencies in some areas. In April 2022, the country prohibited political donations made in cryptocurrencies, citing concerns about potential misuse to influence elections. This cautious strategy reflects an effort to integrate digital assets into the broader economy while simultaneously mitigating associated risks.

Market Context

The timing of this report is crucial. Bitcoin (BTC), the leading cryptocurrency, was trading at $62,884 on June 18, 2026, experiencing a 2.09% decline over 24 hours. Global crypto adoption continues to rise, with an estimated 741 million people owning digital assets in 2025—a 12.4% increase from the previous year. Despite ongoing challenges, Ireland's high crypto ownership, coupled with the introduction of new EU tax transparency rules and enhanced regulation, suggests its market is on a path towards maturation.

For investors and crypto businesses operating in Ireland, it is essential to closely monitor upcoming regulatory developments. With nearly five years until the proposed 2027 standards come into full effect, the country's crypto sector is entering a pivotal period of adjustment and scrutiny. This environment demands vigilant adaptation to ensure compliance while capitalizing on the evolving digital asset landscape.

17.06.2026

Trading platform Robinhood to cut 10% of its full-time workforce

Introduction to Robinhood Markets, Inc.

Robinhood Markets, Inc. emerges as a significant player in the financial markets, specializing in the operation of mobile investment and financial services platforms. The company's growth and development have been remarkable in adapting to the ever-evolving needs of both institutional investors and individual investors. Robinhood's mission to democratize finance for all has been evident in its wide range of offerings that appeal to the tech-savvy new-age investor.

Commission-Free Investment Opportunities

Central to Robinhood's appeal is its online investment platform which allows users to invest commission-free. This feature is a game-changer in the trading realm, offering access to stocks, Exchange Traded Funds (ETFs), underlying assets, American Depository Receipts (ADRs), and even shares during Initial Public Offerings (IPOs).

By removing the barrier of fees, Robinhood has made it financially feasible for individuals at various income levels to participate actively in the financial markets. This democratization of investment opportunities leads to a broader market participation, fostering financial literacy, and investing among younger generations.

Seamless Financial Transaction Services

Robinhood's platform goes beyond just offering investment products. The company facilitates automated transfer services of financial securities from third-party trading accounts to the Robinhood trading venue. This ensures that clients can have a consolidated view of their financial holdings in one accessible platform, easing the management of investments.

Venturing into Cryptocurrency Trading

Understanding the rising interest in digital currencies, Robinhood Markets, Inc. also operates a dynamic cryptocurrency trading platform. Currently, it supports real-time trading for eight cryptocurrencies, including popular names such as Bitcoin, Bitcoin Cash, Bitcoin SV, Dogecoin, Ethereum, Ethereum Classic, and Litecoin.

The integration of cryptocurrencies into their trading platform signifies Robinhood's intent to provide a holistic investment experience that caters to modern investment trends. By offering cryptocurrencies, Robinhood captures a segment of the market that is increasingly looking for diversified investment opportunities beyond traditional securities.

Premium Services and Features

To cater to users seeking advanced tools, Robinhood offers a premium subscription service that provides enhanced features. Subscribers can gain advantages such as instant access to deposits, access to in-depth research reports on approximately 1,000 stocks via Morningstar, comprehensive Nasdaq stock data, margin investing, and securities lending.

These premium offerings are tailored to meet the needs of more seasoned investors who require detailed insights and enhanced trading capabilities to pursue sophisticated investment strategies.

Cash Management Services

Besides the investment and trading services, Robinhood also extends cash management services to its users. This inclusion expands the financial utility delivered by Robinhood, making it a one-stop-shop for financial activities and management.

Revenue Streams Diversification

Robinhood's financial robustness is supplemented by its diversified revenue streams. The breakdown includes revenue from transactions at 58.8%, primarily driven by trading in stock options, cryptocurrencies, and equities. The company also garners net interest income (accounting for 37.6% of revenues) derived from activities such as margin lending, securities lending operations, and cash management. An additional 7.4% of revenue comes from other sources.

Conclusion: A Major Player in Financial Markets

By the end of 2025, Robinhood Markets, Inc. showcased a significant milestone, managing USD 322.1 billion of assets under custody for approximately 27 million monthly active users. This accomplishment highlights Robinhood's expanding footprint in the financial industry and its effective market penetration strategies.

Through its innovative platform and comprehensive service offerings, Robinhood has redefined how millions approach investing, making financial markets accessible to a broader audience. Its continued growth and development suggest a promising future as the company continues to align with emerging investment trends and evolving client needs.

15.06.2026

Bitcoin at $66K as US-Iran Deal Revives Risk Appetite

Crypto Market Capitalization and the Influence of Geopolitical Developments

The recent surge in the crypto market capitalization, rising by 1.8% to reach $2.24 trillion, has been notably influenced by geopolitical events, specifically a preliminary agreement between the US and Iran aimed at ending ongoing conflicts. This development has notably increased risk appetite among investors, pushing the crypto market towards the upper boundary of the established upward trading channel, which has been in place since June 6.

Technical Analysis and Market Sentiment

From a technical perspective, cryptocurrencies have found solid support after touching the 200-week moving average. This is a strong indicator that the long-term positive outlook for the market remains intact. However, the short-term analysis presents a different picture, suggesting that the current market recovery up to $2.30 trillion might merely be a corrective bounce following the downturn observed since the highs achieved in May. This scenario underlines the importance of distinguishing between short-term corrections and long-term trends.

Bitcoin's Current Trading Landscape

Bitcoin, the market leader, is currently trading near the $66,000 mark, reflecting a 2.4% increase over the past 24 hours. This recovery positions it near the lows experienced in February-April, offering a critical test for bullish market participants. Should the recovery stall at these levels, it could indicate that the rebound is nearing its end, potentially leading to further price declines. Conversely, if the previous support does not reverse into a resistance, it could significantly bolster bullish sentiment and catalyze further price increases in the days ahead.

Market Dynamics and Investor Sentiments

The latest data from SoSoValue reveals an interesting development: net weekly outflows from spot Bitcoin ETFs have decreased to $316 million, down from a previous record high. This change signifies a glimmer of renewed investor interest, as evidenced by the first inflow recorded after nearly a month of consistent outflows. However, JPMorgan notes a decline in investors' use of Bitcoin and gold as traditional hedges against the depreciation of fiat currencies, indicating a shift in investment strategies.

Bitcoin's Correction Phase and Market Cycle Indicators

According to Glassnode, Bitcoin appears to be in a late-stage correction phase. Many recent buyers are experiencing losses, and overall demand remains weak, not aligning with levels typically seen at the formation of a long-term market bottom. Galaxy Research's analysis supports this, with only four out of 13 key indicators suggesting a market bottom. They predict possible price declines, potentially reaching the $40,000 to $46,000 range.

Cost of Mining and Long-Term Investment Prospects

Currently, Bitcoin's trading price aligns closely with its mining cost of approximately $61,200, where electricity comprises around $49,000 of these costs. Capriole Investments suggests that a long-term market bottom may form near this cost level. Standard Chartered concurs, asserting that Bitcoin has already established a cycle bottom just above $59,000 and that the market is setting the stage for a new growth phase, offering attractive entry points for long-term investors.

Recent Adjustments in Bitcoin Mining Difficulty

A significant adjustment in Bitcoin's mining difficulty has taken place, with a decrease of 10.09% to 124.93 T. This marks the largest decline in this metric since early February, underscoring the impact of external factors, such as adverse weather conditions, on the mining environment. This adjustment reflects the dynamic nature of the crypto ecosystem and its susceptibility to both internal and external influences.

Conclusion

The current crypto market scenario presents a complex interplay of technical, geopolitical, and investor sentiment factors. While the long-term outlook remains positive, the short-term corrections warrant cautious consideration. As always, it is crucial for investors to stay informed and adaptable, responding to the evolving market conditions with a strategic balance of risk and opportunity.

12.06.2026

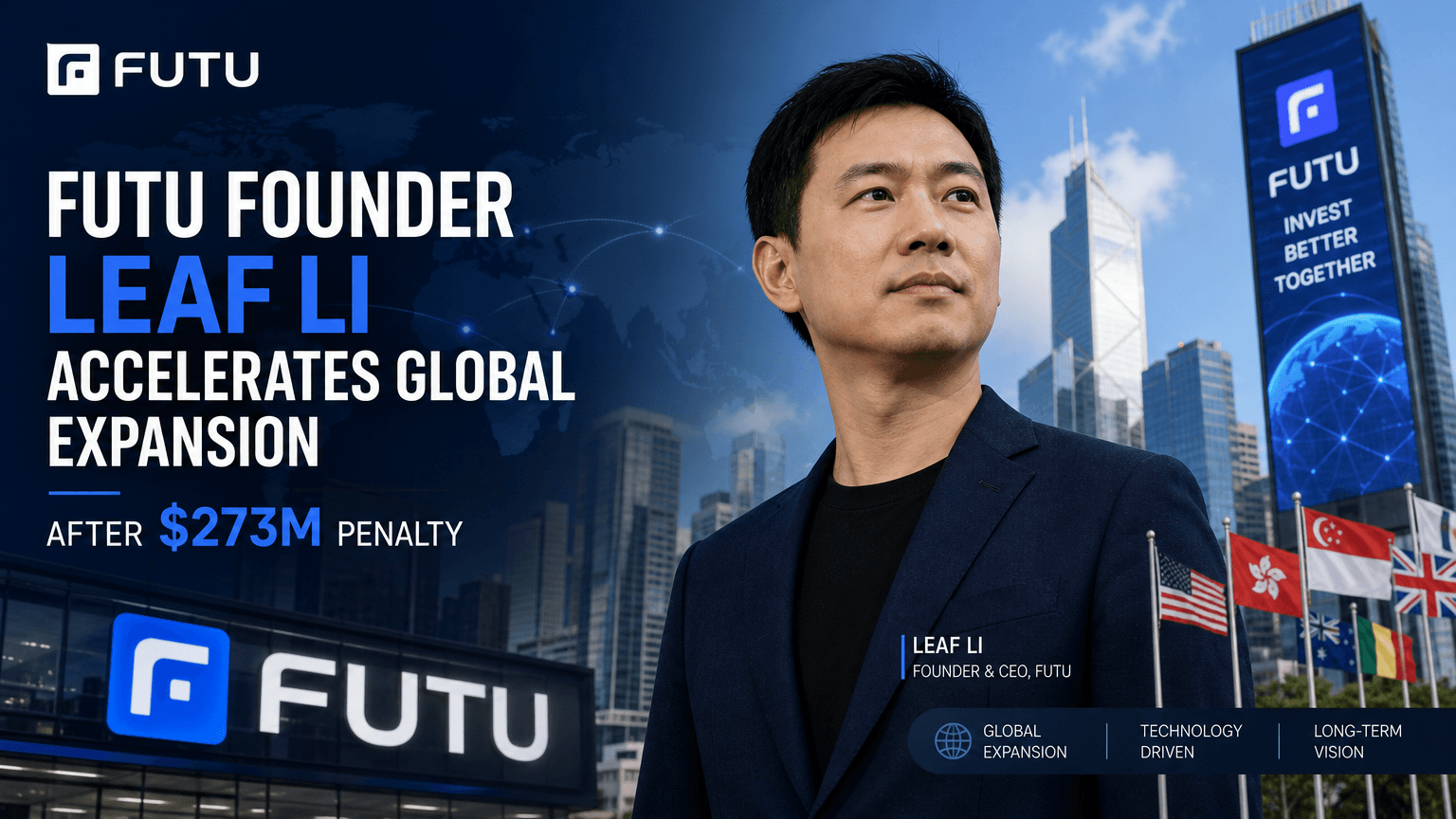

Futu founder Leaf Li accelerates global expansion after $273M penalty

Futu Holdings' Global Ambitions amid Regulatory Challenges

China's securities regulator has targeted Futu Holdings with a substantial fine for unlicensed trading activities. Yet, what might seem like a significant setback is part of a pre-existing strategic pivot by the company towards international markets. This ambitious strategy aims to dilute reliance on Futu's home market and reduce exposure to China's stringent regulatory environment, showcasing the foresight of founder Leaf Hua Li.

The Regulatory Clampdown

On May 22, the China Securities Regulatory Commission (CSRC), along with its Shenzhen bureau, proposed a hefty administrative penalty amounting to around $271-$273 million. These charges stem from allegations that Futu was engaging in unlicensed securities and futures business activities targeting clients from mainland China. Additionally, Leaf Hua Li, the company's founder, was hit with a personal fine of RMB 1.25 million. This significant blow, however, is being met with a robust international strategy which was already in progress.

Navigating Through Numbers

Futu's strategic pivot is reinforced by compelling financial data. Today, mainland Chinese clients constitute a mere 13% of the company's total funded accounts. Conversely, international clients, served primarily through the Moomoo brand, now represent over 55% of Futu's client base. The company’s Q1 2026 financial metrics emphasize growth and resilience despite regulatory scrutiny. With a substantial revenue of $746.9 million, marking a 25% increase year-over-year, and a remarkable rise in total client assets to $155.8 billion, the company is clearly reaping the benefits of its international expansion.

Expansion into Cryptocurrency

Futu's global expansion strategy isn’t confined to traditional securities. In a world growing increasingly digital, Futu has ventured into the realm of cryptocurrencies. Through its PantherTrade platform, the company is pioneering licensed virtual asset trading in Hong Kong, offering an innovative blend of cryptocurrency trading services combined with integrated securities financing options. This diversification aligns with global investment trends and sets Futu apart in a competitive financial landscape.

Market Dynamics and Investor Considerations

Unsurprisingly, Futu's stock experienced a tumultuous period following the penalty announcement, with variations ranging between an 8% and 37% drop. Similarly, Li's personal net worth witnessed a decline from its previous estimation of around $7.6 billion. Yet, when placed in broader financial context, the penalty equates to about a third of a single quarter's revenue. Given the company's robust financial health, represented by $155.8 billion in client assets, the penalty is a significant but not fatal blow.

Implications for the Broader Fintech Sector

Futu's experiences are a cautionary tale for other Chinese fintech companies operating in the realm of cross-border financial services. The CSRC’s stringent measures underscore a broader regulatory tendency towards heightened scrutiny on businesses that blur the line between domestic and international markets. As Futu demonstrates, strategic diversification and international market engagement could be both a buffer and a growth pathway for companies operating under similar pressures.

Conclusion: The Road Ahead for Futu Holdings

Futu Holdings stands as a compelling case study in turning regulatory challenges into opportunities for strategic expansion. Through diversification into international markets and innovative sectors like cryptocurrency, the company is not merely surviving but thriving. As the financial climate continues to evolve, Futu's experience offers valuable insights for other businesses navigating similar landscapes. Future vigilance and adaptability remain paramount as companies like Futu forge paths toward sustainable growth and global financial success.

10.06.2026

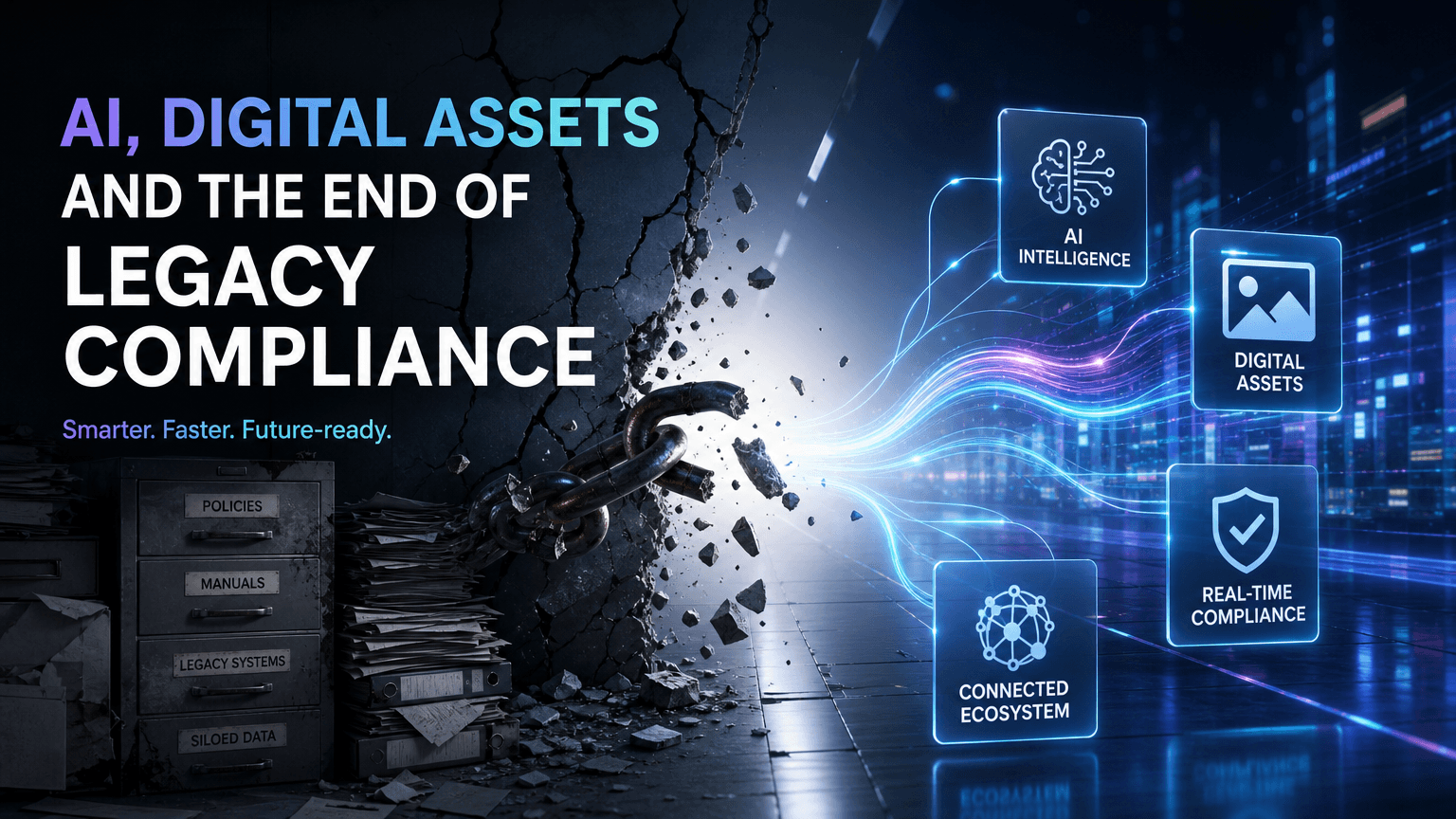

AI, digital assets and the end of legacy compliance

The Transformation of Compliance in Global Banking

Compliance has transitioned from a peripheral function within the back office to a central component in the boardroom strategy for global banks. It has evolved from a quiet operational component to a dynamic and influential element that shapes how financial institutions handle growth, adopt new technologies, regulate employee behavior, and meet increasing regulatory demands across various jurisdictions. This marked shift indicates the escalating importance of compliance in the modern banking sector and its impact on the overall strategic operations of banks.

Navigating the Complex Landscape of Global Risk and Regulation

According to insights from StarCompliance, the challenge facing global banks goes beyond the sheer volume of regulations. The entire operating landscape has become more interwoven, causing traditional compliance risk management structures to lag behind. StarCompliance recently highlighted three critical areas: global risk, the governance of artificial intelligence (AI), and regulatory pressure.

Financial institutions are currently managing several simultaneous challenges, including expectations surrounding AI governance, oversight of digital assets, meeting operational resilience requirements, enforcing sanctions, adjusting to evolving accountability frameworks, and navigating an intricate tapestry of regional regulations. The convergence of these pressures, arriving simultaneously rather than sequentially, presents diverse supervisory expectations unique to each market, creating an acute situation for banks to address.

The Challenge for Compliance Teams in Fostering Innovation

For compliance teams, this climate poses an ongoing balancing act. They are tasked with enabling innovation and facilitating business growth while demonstrating effective governance, maintaining defensible oversight, and achieving real-time risk visibility across the organization. These objectives must be met amid increasing complexity and regulatory scrutiny.

Transitioning from Traditional Compliance Models

Traditionally, many banking compliance programs were designed for more centralized and predictable regulatory environments. However, that model is now under strain. Financial institutions are processing larger data volumes, managing employee activities across numerous markets and digital platforms, and facing increasingly intricate reporting obligations. Simultaneously, regulators are emphasizing active demonstration of compliance controls versus merely having policies exist on paper.

This shift compels banks to fundamentally reassess their compliance infrastructure. Disconnected systems, fragmented reporting, and manual oversight processes introduce operational delays and leave institutions vulnerable when regulators request evidence, escalation histories, or audit trails at short notice. Consequently, compliance technology, governance, and data management are being reconsidered at an enterprise level.

The Role of Artificial Intelligence in Compliance

Artificial intelligence is accelerating this transition. Banks are increasingly exploring AI-driven surveillance, monitoring, and risk detection tools. However, this comes with heightened scrutiny from regulators regarding governance, accountability, explainability, and model oversight. For compliance leaders, the focus has shifted from debating AI deployment to determining responsible usage within existing regulatory frameworks.

Expanding the Risk Perimeter with Digital Assets and Employee Conduct

The intersection of traditional finance and digital assets represents another significant shift. Activities like cryptocurrency trading, tokenized assets, decentralized finance platforms, and prediction markets introduce new risks concerning employee conduct and information that existing surveillance programs were not originally designed to capture.

This is especially critical for global financial institutions, where escalating regulatory focus is on conflicts of interest, material non-public information, and employee trading activities that extend beyond traditional brokerage accounts. Compliance programs require visibility across more financial activities, necessitating technology that can adapt to evolving market structures.

Adapting to a Connected Compliance Approach

As regulatory complexity intensifies, many banks are gravitating towards more centralized and connected compliance operating models. The emphasis is shifting towards integrating governance, surveillance, employee disclosures, case management, reporting, and audit documentation into cohesive frameworks that can scale globally while accommodating regional regulatory demands.

StarCompliance has positioned itself at the forefront of this shift. For over 25 years, StarCompliance has collaborated with financial institutions worldwide to manage employee compliance, conflicts of interest, personal account dealings, gifts and hospitality oversight, political contributions, external business activities, and information barrier controls through connected compliance technology.

As banks continue to overhaul their compliance infrastructures, technology's role has become a fundamental operational necessity for managing risk consistently across jurisdictions. Rather than supporting function, technology has become integrally embedded within the compliance landscape, underscoring the evolution from traditional models to more dynamic, interconnected systems in global banking.

08.06.2026

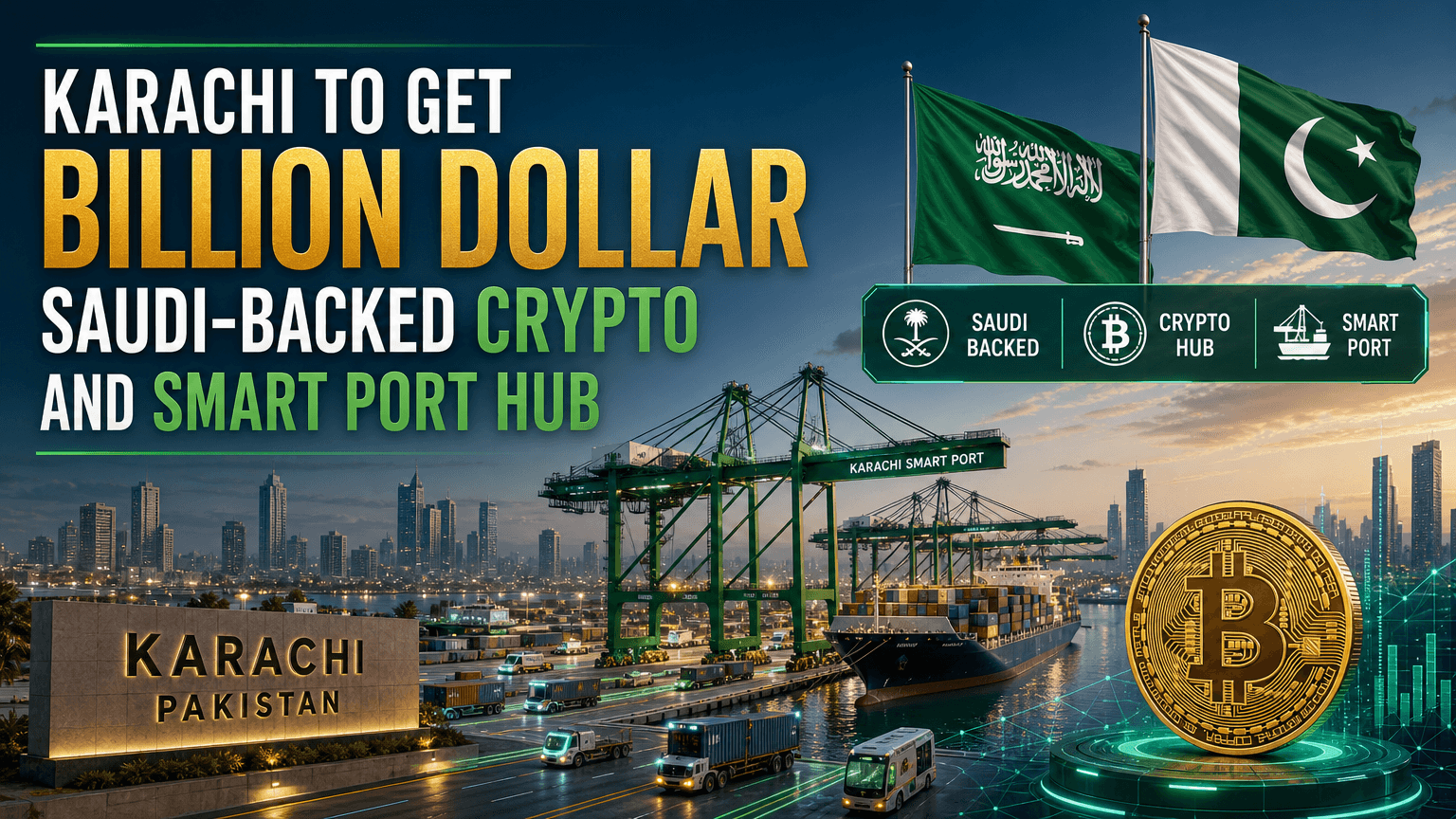

Karachi to get Billion Dollar Saudi-Backed Crypto and Smart Port Hub

Karachi's Waterfront Transformation: A New Frontier for Innovation and Trade

Karachi, Pakistan's bustling financial epicenter, is on the cusp of a transformative development. A significant stretch of port-owned land is poised to evolve into a vibrant hub of innovation, digital finance, and global commerce, thanks to a groundbreaking partnership between Pakistani and Saudi investors. This ambitious initiative is set to not only revolutionize the city's skyline but also redefine how Karachi engages with the global economy.

The Dynamics of the Partnership: A Synergy of Vision

The collaboration involves key stakeholders, including Saudi investors joining forces with notable Pakistani partners. Together, they aim to explore the creation of a sprawling cryptocurrency and blockchain zone in the thriving port city. This development will be complemented by a digital banking hub, smart port infrastructure, luxury real estate projects, and major healthcare and education facilities.

Memorandum of Understanding: Paving the Way Forward

The foundation of this groundbreaking initiative was laid with the signing of a memorandum of understanding (MoU) involving the Karachi Port Trust (KPT), the Saudi Business Council-Najd Gateway Holding Company, Arif Habib Dolmen REIT Management Limited, and the Pakistan Corporate Consortium. The MoU sets the stage for a collaboration that promises to bring unprecedented growth and development to Karachi's waterfront.

Project Scope: A Vision for a New Coastal Landscape

The proposed development encompasses approximately 140 acres of prime KPT-owned land on Moulvi Tamizuddin Khan Road. The plan is to transform this site into a modern commercial and maritime district that can attract regional and international investors. This ambitious project signals South Asia's increasing efforts to regulate digital assets and cryptocurrency trading, positioning Karachi as a nexus for financial innovation.

Comprehensive Urban Development: Blending Commerce with Technology

Plans for the area include a marine technology and logistics zone, smart port integration systems, digital customs services, and maritime software development projects. These initiatives aim to modernize Pakistan's shipping and port operations. Broadly, the vision incorporates international-standard hospitals, a medical university, a maritime and trade law school, luxury hotels, skyscrapers, corporate headquarters, and a large convention center.

Strategic Developments and Economic Potential

This announcement aligns with a recent visit by a Saudi delegation to Pakistan, where discussions also included potential ventures like an oil refinery at Gwadar Port and strategic oil storage facilities. The Karachi waterfront project is designed to fulfill all legal and regulatory requirements, aiming to attract investment, stimulate economic activity, and support urban renewal along the city's coastline.

Positioning Karachi in the Global Digital Finance Arena

The proposed crypto-focused district comes at a pivotal time when global competition for digital finance and blockchain investment is intensifying. Proponents believe this project could position Pakistan as a regional destination for technology-driven capital, strengthening ties with Gulf investors and fostering economic synergy.

The Rise of South Asia's Largest Integrated Waterfront Development

Should plans progress beyond the proposal stage, Karachi could soon witness one of South Asia's largest integrated waterfront developments. This mega project aims to combine cryptocurrency, digital banking, smart ports, energy, education, healthcare, and luxury real estate into a cohesive and prosperous urban environment.